The Role of Accounting Learning in Forming Anticorruption Character at SMK Negeri 1 Banjarmasin

DOI:

https://doi.org/10.23917/jpis.v33i2.2949Abstract

This research aims to determine the role of accounting learning in forming anti-corruption character at SMK Negeri 1 Banjarmasin. The research method used in this research is an experimental method using a quantitative research approach. The research subjects were 135 class XII students of the institutional financial accounting skills program. The sampling technique used in this research was purposive random sampling. While the data collection technique is through questionnaires and documentation, the data analysis used in this research is a structural model or inner model by calculating R-Square or coefficient of determination (R2), path coefficient estimation, and Hypothesis Testing (re-sampling and bootstrapping). The results of data analysis show that there is a positive and significant relationship between the role of accounting learning and the formation of anti-corruption character. This research is the initial stage in triggering students' anti-corruption character.

Downloads

INTRODUCTION

Corruption is a serious problem that is detrimental to society and the country in general. The impact of corruption can be felt in various aspects of life, such as economic, political, social and moral. Corruption harms a country's development by hampering economic growth, creating social injustice, weakening good governance systems, and reducing public trust in the government and public institutions. To eradicate it, it is not enough just to carry out repressive measures, but there needs to be more basic efforts by carrying out preventive or preventative measures (Anesti, Darmawani, & Ramadhani, 2022). Efforts to prevent acts of corruption can be done by early prevention of acts of corruption through education (Siswanto, Suyanto, & Kartowagiran, 2017). Great attention to character education is carried out to place character education in its true proportions so that the young generation is not only intelligent and knowledgeable but also a generation with morality and good character, especially anti-corruption character (Noor, 2020). Instilling anti-corruption values in schools is an effort to instill moral values in students and anticipate the occurrence of corrupt practices in the future among new generations (Pahlevi & Fahmi, 2022).

In the problem of eradicating corruption, the world of education is expected to be able to prevent corruption from an early age (Suryani, 2015). Learning with character values is learning that leads to strengthening and developing student behavior as a whole based on a value (Yunitia & Hakim, 2014). According to Toni Nasution, character is values that are uniquely good and have a good impact on the environment and are manifested in a person's behavior (Nasution, 2018). Handoyo (2007) revealed that: anti-corruption education is a conscious effort to provide understanding and prevent corruption in the learning process at school (in Gandamana. 2018). According to Gurning, Mudjiman & Haryanto, anti-corruption education is an effort to prevent acts of corruption by providing students with an understanding of the ins and outs of corruption that can be carried out in the learning process at school (Suryaningtyas, Siswandari & Hamidi, 2019).

Anti-corruption character education in the implementation of learning is carried out so that students can connect the subject matter with real life, which can make students understand knowledge better which not only emphasizes cognitive aspects but also affective and psychomotor, so that students are expected to be able to have skills that can be used in everyday life (Rahmawat, Wardani, & Noviani, 2016). Anti-corruption education is a conscious effort to provide understanding and prevention of acts of corruption carried out through formal education in madrasas, informal education in the family environment and non-formal education in the community (Nuryati, Budiutomo, & Bowo, 2017). One learning that can be integrated with an anti-corruption character is accounting learning.

As a science, according to Nafarin (2015), accounting learning is a scientific discipline that studies mechanisms, systems and procedures in recording, classifying, summarizing and interpreting financial transactions that occur in an organization's data and are expressed in monetary value (Siswanto, 2020). Accounting learning has an important role in forming an anti-corruption character. Accounting is an information system used to measure, record and report the financial activities of an entity. Through studying accounting, individuals can understand the importance of integrity, transparency and accountability in managing financial resources. Accounting plays an important role in generating relevant and reliable information for economic decision making. By positioning accounting as a preventive activity then Students will have an understanding that anti-corruption education does not only concern political matters, but also people who have the potential to commit corruption if the recording/bookkeeping is not done well (Siswanto, 2020). The accounting profession in the financial sector is the heart of companies that deal with rupiah or currency, so it is close to corruption. Thus, the implementation of anti-corruption education in the realm of education, especially accounting, needs to be updated, managed and implemented optimally to create generations free of corruption (Wahab, Sahade, & Samsinar 2022).

Accounting requires accuracy, honesty, discipline, independence and responsibility, which are the dominant characteristics of accounting. Character formation in accounting subjects can start from knowledge of the character values contained in accounting material (Fitriyati, 2017). In accounting learning that integrates anti-corruption characters, five characters emerge, namely (1) honesty, (2) responsibility, (3) discipline, (4) hard work, and (5) courage (Kristiono, Uddin, & Astuti, 2021). Accounting learning is one of the competencies in vocational schools that prepares students to have the competency to carry out financial recording activities in service, trading and manufacturing companies (Siswanto, Suyanto, & Kartowagiran, 2017).

Accounting learning can be interpreted as a series of learning procedures which aim to enable students to apply accounting methods based on scientific principles. Students are expected to be able to understand the importance of accounting as a business language in making decisions for the sustainability of an entity and preparing financial reports according to predetermined competency standards. Accounting learning is carried out by implementing supporting learning strategies so that learning activities can take place effectively and efficiently. Accounting learning is mostly carried out using traditional methods with a teacher-centered system because accounting is a procedural science that has standardized concepts both nationally and internationally (Dwiharjo, 2015). In its implementation, character education can be integrated where teachers are required to care, be willing and able to relate character education concepts to accounting learning (Agustina, 2015). Accounting students in vocational schools are students who are prepared to work in the financial sector, especially as bookkeepers (Suprapti, Priono, Thamrin, & Baso, 2021).

SMK Negeri 1 Banjarmasin is one of the schools that has a major in institutional financial accounting. Based on the results of an interview with one of the teachers there, the process of intensifying student character integration is still in the normal category. There is still no complete, complete, perfect integration of the characters. By integrating character into accounting learning, it is hoped that students will be created who are not only intelligent but also have character. The accounting learning process that integrates anti-corruption characters is predominantly influenced by teachers, lesson plans, school leadership and school culture (Siswanto, Suyanto, & Kartowagiran, 2017).

Based on the interview results, specific support for integrating character into learning is still lacking. The characteristics of learning at SMK Negeri 1 Banjarmasin tend to be practical because students are work-oriented. Therefore, there is a need for character education that is specifically shown to vocational school children, which is delivered logically, democratically and holistically. So that accounting students can become good human resources, especially in terms of behavior and attitudes, it is very important to shape their character (Suprapti, Priono, Thamrin, & Baso, 2021). This research is supported by previous research conducted by Siswanto (2020) which states that anti-corruption education is a program whose main mission is to develop and increase students' understanding of the risks posed by acts of corruption. Anti-corruption education will have an important meaning for students by positioning accounting as a preventive activity. Students will have an understanding that anti-corruption education is not just a political issue but is a problem for all of us because they are people who have the potential to commit corruption if the recording or bookkeeping is not done properly. Based on the background presented above, the author is interested in further research regarding the role of accounting learning in forming anti-corruption character at SMK Negeri 1 Banjarmasin.

RESEARCH METHOD

This research was carried out at SMK Negeri 1 Banjarmasin. Experimental methods utilizing quantitative research strategies were applied to the research methodology of this study. Experimental research is a research method used to find the effect of certain treatments on others under controlled conditions (Sugiyono, 2015). Two classes—the experimental class and the control class—were used in the experimental method investigation. Group discussions and case study learning approaches will be used in the experimental class, while more traditional teaching approaches will be used in the control group. The experimental process is carried out by providing material about Accounting learning related to Anti-Corruption Character. After providing the material, students are divided into several groups to analyze case studies and after that they will present the results of their discussion and then study together the results that have been submitted. The case study taken is a case study that could occur in an accounting opening carried out by an accountant. A saturated sampling approach was used as the sampling methodology in this investigation. Purposive random sampling was used as the sampling strategy in this investigation. Meanwhile, surveys and documentation are one method of data collection. The survey developed in this research was carried out by distributing questionnaires with questions related to the anti-corruption character of accounting students at school. The documentation method is carried out by carrying out a direct agenda to see how Accounting is taught at SMK Negeri 1 Banjarmasin, specifically Class XII. This results in document data in the form of how to learn Accounting, what the students' character is, and what anti-corruption characteristics the students have indirectly implemented. All participants in this research were registered in the institutional financial accounting skills program for classes X to XII, with a sample of 135 students in class XII of the institutional financial accounting skills program, divided into two classes, namely the control class (XII). A AKL) and experimental classes (XII B, C, and D AKL). The data analysis used in this research is a structural model or inner model by calculating the R-Square or coefficient of determination (R2), estimating the path coefficient, and hypothesis testing (resampling and bootstrapping).

RESULTS AND DISCUSSION

Results

In this research, it was carried out using the experimental method where the research was carried out by being given different treatment between the control class and the experiment class. The experimental class will be treated with case study and group discussion learning methods and the control class will be treated with conventional learning methods. Experimental class students will receive Accounting learning material which includes Anti-Corruption Character. After being given the material, students will form groups to discuss case studies of corruption that can occur in openings carried out by an accountant. After analyzing the case study they will present the results of their discussion, which will be discussed together with the results of the group discussion led by the researcher.

R-Square

The ability of the structural model to predict outcomes was evaluated using R-Square. To find out whether certain exogenous latent factors have a significant influence on endogenous latent variables, R-Square is used. An R2 valueof 0.75 is considered a strong model; the R2 range is 0.50, which is considered a moderate model; and the R2 rangeis 0.25 which is considered a weak model (Ghozali & Latan, 2015).

Table 1.

R-Square

Source: Primary data processed in 2023

Table 1. shows the results of the R-Square test, where Y has a value of 0.272 which is classified as a weak model. This value shows that the variables honesty (X1), discipline (X2), responsibility (X3), hard work (X4), and courage (X5) have an effect of 27.2% on the accounting learning outcome variable (Y). And the rest is influenced by other variables outside the variables in this research.

Estimate the Path Coefficient

By examining the parameter coefficient values and the t-statistical significance values obtained using the bootstrapping approach, the significance of the influence between variables in this test can be determined. The following table displays the results of this research.

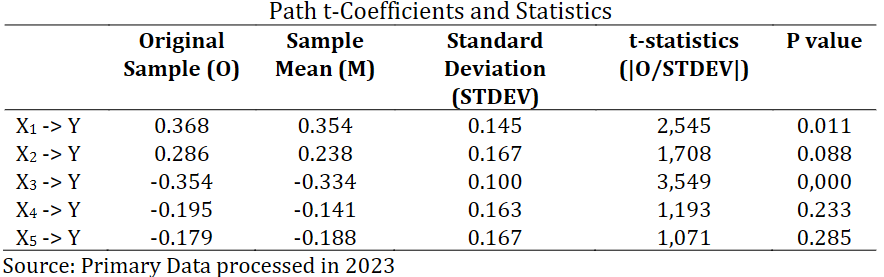

Based on table 2. of the t-statistic coefficients and paths in the table above, it can be said that the highest path coefficient value is found in the relationship between honesty (X1) and accounting learning (Y), which is 0.368. Meanwhile, the lowest path coefficient value is found in the relationship between responsibility (X3) and accounting learning (Y) which is -0.354.

The character of honesty has a higher coefficient relationship because the character of honesty is a basic character that an accountant must have. Students' honest character is always implemented in accounting learning when students record financial reports. Meanwhile, the character of responsibility has the lowest coefficient relationship because the character of responsibility carried out by students is responsibility towards themselves; the character of responsibility towards other people or the environment is still lacking, and they do not realize the importance of responsibility as a student.

Hypothesis Testing (Resampling Bootstrapping)

To test the hypothesis, the bootstrapping technique produces t-statistic values for each association path. The t-statistical and t-table values will be compared. The t-table value can be determined based on a confidence level of 90%, 95%, or 99%. When using a 95% confidence level, the precision or inaccuracy limit (a) is 5% or 0.05 (Ghozali & Latan, 2015).

The indicator validity test is analyzed using degrees of freedom (df) with the formula: df = n – k (Hudin & Riana, 2016). The number of observations in this study was 101, while the number of variables studied was six. So the result is df = 101 – 6 = 95. For the t-table value with a significance level of 5% using a two-way test and degrees of freedom 95 = 1.985.

Based on table 2. coefficients and t-statistics paths in the table above it can be said that H1 accepted: Based on the research results, the influence of honesty (X1) and accounting learning (Y) in the experimental class is positively and significantly correlated. The initial sample size of 0.368 reveals the direction of the relationship. The t-statistic value of 2.545 which is greater than the t-table of 1.985 shows significance. The research p value of 0.011 also meets the established criteria, namely 0.05. This shows that the experimental class at SMK Negeri 1 has a positive and significant effect on the quality of accounting learning and the development of students' honesty and character.

H2 rejected: Based on research findings, the influence of discipline (X2) and accounting learning (Y) in the experimental class has a positive but negligible relationship. From the initial sample of 0.286, the direction of the relationship can be determined. The fact that the t-statistic is 1.705, which is smaller than the t-table of 1.985, is not significant. Apart from that, the research p value of 0.088 also does not meet the set criteria, namely 0.05. This shows that the experimental class at SMK Negeri 1 Banjarmasin has little or no influence on the quality of accounting learning in terms of forming students' disciplinary character.

H3 accepted: The research results show that in the experimental class there is a negative and substantial relationship between the influence of responsibility (X3) and accounting learning (Y). The original sample of -0.354 reveals the direction of the relationship. The t-statistic value of 3.589 is greater than the t-table value of 1.985, indicating significance. The research p-value of 0.000 also meets the established criteria, namely 0.05. This shows that the experimental class at SMK Negeri 1 Banjarmasin has a negative and significant effect on the quality of accounting education in developing student responsibility.

H4 rejected: Based on research findings, the influence of effort (X4) and accounting knowledge (Y) in the experimental class has a bad relationship and is not important. The original sample of -0.195 shows the direction of the relationship. The t-statistic value of 1.193 is smaller than the t-table of 1.985, indicating that the difference is not significant. The research p value of 0.233 is also below the threshold set at 0.05. This shows that the experimental class at SMK Negeri 1 Banjarmasin is still not significantly impacted by the effectiveness of accounting learning in developing students' diligent character.

H5 rejected: According to research findings, the influence of courage (X5) and accounting learning (Y) in the experimental class has a good but negligible relationship. The original sample of -0.179 shows the direction of the relationship. The t-statistic value of 1.071 is smaller than the t-table of 1.985, indicating that the difference is not significant. The research p value of 0.285 is also below the threshold of 0.05. This shows that the experimental class at SMK Negeri 1 Banjarmasin has not yet had a significant impact on the quality of accounting learning in terms of developing students' courage and character.

Discussion

Based on the research results described above, the role of accounting learning in integrating anti-corruption character with methods and plans that have been prepared to form this character is better than character formation without methods and plans that have not been prepared. The results of the research show that the school environment and accounting teachers at SMK Negeri 1 Banjarmasin understand character education and the process of character formation for SMK Negeri 1 Banjarmasin students. Students practice character in the school environment by complying with applicable regulations, and those who violate will be subject to sanctions according to the type of violation. This can be said to integrate the characters indirectly, but even so their initial knowledge about the characters in general can be said to be quite good.

From the results of the SmartPLS test in the experimental class, there are two characters that have a good influence on students' character development. Even though the other three characters have not been able to have a significant influence, research on these characters shows that they can be the initial stage in triggering the emergence of better characters. Meanwhile, in the Contorul class, there was only 1 student character that had a good influence on their development in learning accounting and 4 student characters that had not had a good influence on their development in learning accounting.

Experimental class students learn using case study learning methods and group discussions. Students can play an active role in learning. Meanwhile, students in the control class use conventional learning methods where students are more likely to listen to explanations related to the character of anti-corruption itself in learning accounting. So even though they are given the same material at the same time, in the case study and discussion methods students are trained to look for and discover existing problems, as well as discussing among group members or active discussions between groups commanded by the teacher himself, making them more can know and understand the character of anti-corruption. So that after that it can be implemented regularly so that students can better master and apply the anti-corruption character in everyday life. This will also provide provisions for them to act as good accountants and with character.

This is in line with the results of research from Rahmawati, Wardani, & Noviani, (2016) who said that the implementation of integrated character education in learning includes three stages, namely the planning, implementation and evaluation stages. Teachers must include character values in the plans made before carrying out learning activities. By integrating character values into planning, implementation will be more focused and effective.

The cognitive domain emphasizes the formation of knowledge and understanding regarding corruption and other aspects. The affective domain leads to changes in students' perceptions and attitudes towards corruption. Meanwhile, the psychomotor domain emphasizes the aim of training skills and abilities to fight corruption (Altakiyah, 2017). Development of accounting learning which is learning that not only contains knowledge (cognitive) but also contains attitudes (effectiveness) and skills (psychomotor). The integration of anti-corruption character in accounting learning carried out in this research is still at the stage of providing knowledge by explaining the anti-corruption character, providing practice questions, analyzing problems and solving problems in case studies in discussions, so that in this research it has not yet reached the stage where students can be said to be able to do it. implement it.

The integration of anti-corruption character in accounting learning carried out in this research is still at the stage of providing knowledge by exposing anti-corruption character, providing practice questions, problem analysis, and solving problems in case studies in discussions, so in this research it has not yet reached the stage where students can be said to be capable implement it. In this research, it is still small in scope, where only the scope of the relationship between teachers and students in accounting learning has not yet reached the stage of empowering the entire potential of existing schools. However, this research can show the initial stage to which students know the character of anti-corruption.

The initial stage of integrating anti-corruption character in accounting learning for students at SMK Negeri 1 Banjarmasin is to find out the extent of students' initial knowledge about anti-corruption character which can be seen by giving a questionnaire about anti-corruption character with positive results and significant impact. And accounting learning itself is carried out using the case study method, and discussions are a good initial stage. These results can be said to be good because from the results of direct observation the value of the results of the training changes has increased the level of understanding which is quite good.

This is also in line with the results of Siswanto's research (2020) which states that anti-corruption education will have an important meaning for students by positioning accounting in preventive activities. Students will have an understanding that anti-corruption education is not just a political issue but is a problem for all of us because they are people who have the potential to commit corruption if the recording or bookkeeping is not done properly.

CONCLUSION

Accounting learning that occurs at SMK Negeri 1 Banjarmasin is carried out with a series of exercises and practices by delivering material through lecture methods and peer visits for students to help each other understand the learning. And accounting learning is supported by computer lab facilities. In the process of character formation at SMK Negeri 1 Banjarmasin, PKN learning occurs as knowledge about character. And the practice of this character can be seen in the actions of students in the school environment in obeying school regulations. The role of accounting learning in forming anti-corruption character in students at SMK Negeri 1 Banjarmasin in testing using SmartPLS shows that the frequency of anti-corruption character indicators with prepared methods and plans has a greater influence than without preparation. This can also be seen from the relatively high student learning outcomes regarding knowledge of anti-corruption characters, and from the test results it was found that two characters had a good influence on their development. Therefore, integrating anti-corruption characteristics requires more mature planning and synergistic efforts in several aspects. This research is limited to a small scope that occurs in the classroom between teachers and students in Accounting learning supported by learning methods. This research does not cover all aspects of the school environment that can support the formation of students' anti-corruption character. For this reason, it is hoped that future researchers can develop existing research to be able to expand the scope of research to the scope of the school environment, not just from the classroom scope that occurs in the classroom between teachers and students.

References

Agustina, S. (2015). Student Character Development Through Contextual Teacher and Learning in Accounting Learning in Vocational Schools (A Theoretical Study). Proceedings of the National Seminar, 23-32

Altakiyah, S. (2017). Application of the Problem Bases Learning Model to Increase Anti-Corruption Values and Accounting Learning Activities. Indonesian Accounting Education Review, 6(2), 1-17.

Anesti, A. Darmawani, E. & Ramadhani, E. (2022). Analysis of the Implementation of Anti-Corruption Education at SMK Negeri 5 Palembang. Journal of Education and Counseling (JPDK), 4(5). 7930-7935.

Dwiharjo, L. M. (2015). Utilizing Edmodo as an Accounting Learning Media. Seminar Proceedings National, 332-344.

Fitriyanti. (2017). Character Values in Accounting Learning. Seminar PGRI National Education. 46-50.

Ghozali & Latan. (2015). Partial Least Squares: Concepts, Techniques and Applications Using the Smartpls 3.0 Program. Semarang: Diponogoro University Publishing Agency.

Kristiono, N. Uddin, H. R., & Astuti, I. (2021) Implementation of Anti-Corruption Values as an Effort to Prevent Corruption at Texmaco Vocational School, Pemalang. Scientific Horizons Journal, 1(4), 619-626.

Nasution, T. (2018). Building Student Independence Through Character Education. UTIMAIYAH, 2(1), 1-18.

Noor, S. R. (2020). Anti-Corruption Character Education as Part of Early Corruption Prevention Efforts in Indonesia. Moralyt: Journal of Legal Studies, 6(1), 55-73.

Nuryati, Budiutomo, T., & Bowo, A. N. A. (2017). Development of an Environment-based Anti-Corruption Civics Education Learning Model Through Cooperative Learning at Private High Schools/Vocational Schools in Kulon Progo, Yogyakarta. Academy of education journal. Faculty of teacher training, and education, 8(1). 27-49.

Rahmawati, A., Wardani, D. K., & Noviani, L. (2016). Implementation of Integrated Character Education in Economics Learning at SMA Negeri 2 Magelang, Jurnal Pendidikan Bisnis dan Ekonomi, 2(1), 1-21.

Pahlevi, P. & Fahmi, I. (2022) The Role of Educators in Instilling Anti-Corruption Values in High Schools. Scientific Journal of Educational Vehicles, 8(16), 44-54.

Siswanto, (2020). Accounting Learning as a Media for Cultivating Anti-Corruption Character. Indonesian Journal of Accounting Education, 18(1), 47-59.

Siswanto, Suyanto, & Kartowagiran. B. (2017). Anti-Corruption Values in Accounting Learning as Student Character Development in Vocational Schools. Journal of Educational Development: Foundations and Applications, 5(1), 75-86.

Sugiyono (2015). Quantitative, Qualitative, and R&D Research Methods. Bandung: Alfabeta.

Suryaningtyas, N., Siswandari & Hamidi, N. (2019). Students' Perceptions of the Value of Independence in Anti-Corruption Education (Studies at Vocational Schools). UNS “Tata Arta" Journal, 5(1). 82-94.

Suryani, I. (2015). Instilling Anti-Corruption Values in Higher Education as a Preventive Effort to Prevent Corruption. Journal of Communication Vision, 14(2), 285-301.

Suprapti, E. Priono, H. Thamrin, E. T., & Baso R. (2021). Character Education in Accounting Learning is an Effort to Form Accounting Students. Tangible Journal, 6(1), 39–54.

Wahab, N. Sahade, & Samsinar. (2022). Understanding Anti-Corruption Education in Accounting Teachers at State Vocational Schools in the Makassar City Accounting Skills Program. Undergraduate thesis, Universitas Negeri Makassar.

Yunita, I. E. & Hakim, L. (2014). Development of Contextual-Based Modules That a Characterized by Special Journal Material. Journal of Accounting Education (JPAK), 2(1), 1-6.

Downloads

Submitted

Accepted

Published

Issue

Section

License

Copyright (c) 2023 Jurnal Pendidikan Ilmu Sosial

This work is licensed under a Creative Commons Attribution 4.0 International License.