Reducing Return Volatility: The Role of Earnings Quality and Corporate Reputation

DOI:

https://doi.org/10.23917/reaksi.v9i1.4653Keywords:

Earning Quality, Stock Return Volatility, Corporate Reputation, Public Company, SEM-PLS.Abstract

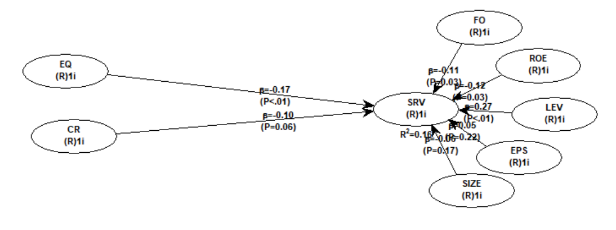

This research aims to explore the influence of earnings quality and company reputation on stock return volatility in non-cyclical consumer companies listed on the Indonesia Stock Exchange (BEI) for the 2017-2021 period using quantitative methods. The research sample was 175 non-cyclical consumer sub-sector companies listed on the Indonesia Stock Exchange (BEI) for the 2017-2021 period and using PLS-SEM. The results of this research found that earnings quality has a negative effect on stock return volatility and company reputation has a negative effect on stock return volatility. Results of this research are expected to be useful for investors when investing in the stock market. Apart from that, it is also hoped that it can also be useful for companies so that they can be more careful in carrying out company operational activities so that they can improve their company's reputation in terms of quality, performance, responsibility and attractiveness which can reduce return volatility. This research is limited to consumer non-cyclicals sector in Indonesia and within just 5 years observation and contributes to existing knowledge by empirically testing the relationship between earnings quality and company reputation on stock return volatility. There has been no research in Indonesia that discusses the influence of company reputation on stock return volatility.

Submitted

Accepted

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Riset Akuntansi dan Keuangan Indonesia

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.