Stickiness of Operating Expense in Asset, Liability, and Income Activities: Evidence from Indonesia

DOI:

https://doi.org/10.23917/reaksi.v10i1.8649Keywords:

sticky cost, operating expense, operating asset, operating liability, operating income 10Abstract

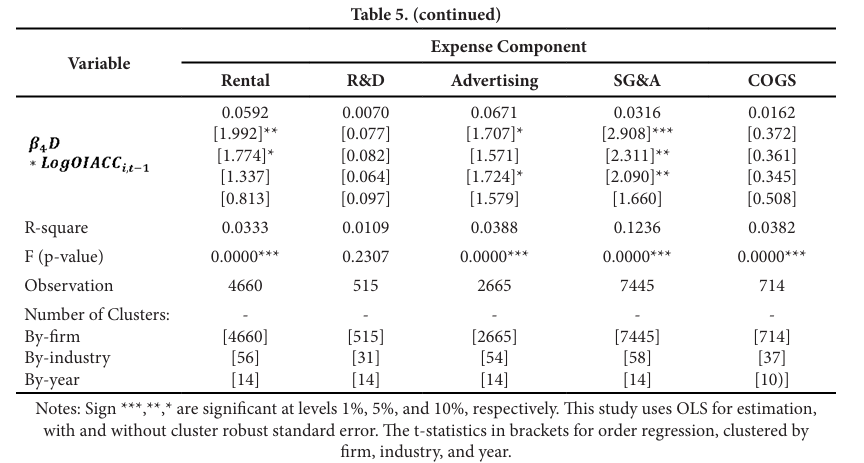

Understanding cost behavior is crucial in accounting management. Sticky costs literature discusses the responsiveness of costs to profits. This study examines the effect of operating expenses, including rental expenses, advertising, R&D, SG&A, and COGS, on operating income, operating assets, and operating liability. The population in this study is listed companies on the Indonesia Stock Exchange. The observation starts from 2010-2023. We use the OSIRIS-Bureau van Dijk Database to generate the data. We analyze the data using OLS regression with cluster robust standard error. We find that the rental, advertising, SG&A, and COGS expenses increase by 10%-14% per 1% increase in operating income. The rental and advertising costs show an estimated value of 33% and 47% per 1% increase in operating assets. Meanwhile, R&D expenses increase by 32% per 1% increase in operating liability.

Submitted

Accepted

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Riset Akuntansi dan Keuangan Indonesia

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.