Sustainability Reporting in Value Creation: The Critical Mediation of Environmental Management Accounting

DOI:

https://doi.org/10.23917/reaksi.v9i3.7030Keywords:

sustainability report disclosure, environmental management accounting, firm valueAbstract

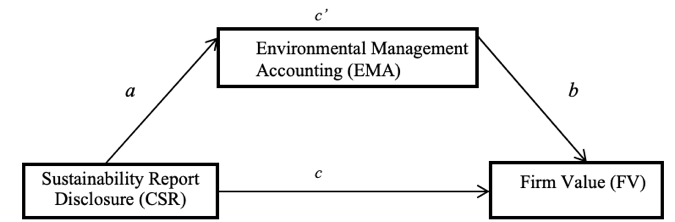

This study examines the essential function of Environmental Management Accounting (EMA) as a mediating variable in the correlation between sustainability report disclosures and firm value. The study highlights the beneficial effects of Environmental Management Accounting (EMA) on value creation by aligning business strategy with sustainable practices, as viewed through the framework of stakeholder theory. Multiple regression and path analyses were performed on a sample of Indonesian manufacturing businesses listed on the Indonesian Stock Exchange (IDX) from 2020 to 2023 to evaluate the assumptions. The findings indicate that EMA substantially increases business value by fostering operational efficiency, transparency, and stakeholder confidence. The Sobel test further substantiates EMA's mediation impact, indicating that organizations with strong EMA procedures get superior financial success and sustainability results. This study highlights the significance of incorporating EMA into sustainability reporting frameworks to improve business value and promote sustainable development.

Keywords: sustainability report disclosure, environmental management accounting, firm value

Submitted

Accepted

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Riset Akuntansi dan Keuangan Indonesia

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.