Implementation of IFRS 17 in the PSAK 108 Revision on Sharia Insurance Transactions in Indonesia

DOI:

https://doi.org/10.23917/reaksi.v9i3.6959Keywords:

IFRS 17, Sharia Insurance Accounting, PSAK 108Abstract

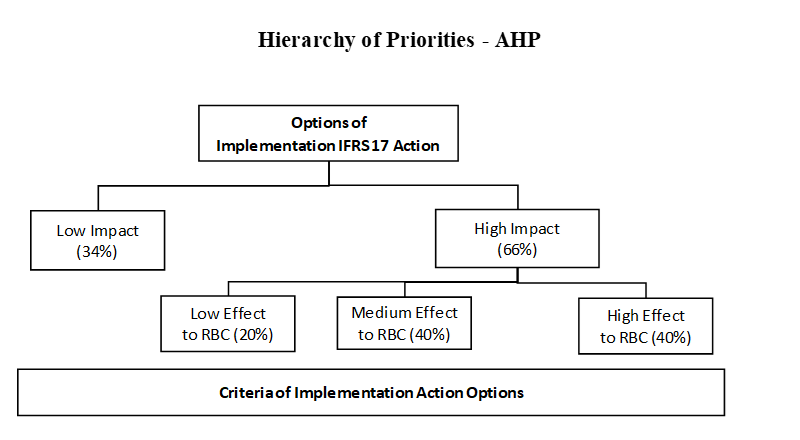

The Sharia insurance industry in Indonesia has shown significant growth, although in the past decade, there has been a decline in contribution growth, particularly in the general Sharia insurance sector. This study aims to analyze the impact of IFRS 17 implementation on the revision of PSAK 108. The research method employed is descriptive analysis using both qualitative and quantitative approaches. Qualitatively, the study applies a descriptive analysis approach through interviews, while quantitatively, it uses the Analytical Hierarchy Process (AHP) method. The findings reveal that 66% of respondents believe that the implementation of IFRS 17 will have a significant impact on the recording, measurement, and presentation of financial statements, with the level of impact varying based on the type of insurance business. Regarding the impact on the RBC (Risk-Based Capital) of insurance companies, 20% indicated a low impact, while 40% reported medium to high impacts. These findings suggest the need for operational system adjustments, capital strengthening, and enhancement of human resource capacity to address the challenges posed by IFRS 17 implementation in Indonesia.

Submitted

Accepted

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Riset Akuntansi dan Keuangan Indonesia

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.