Enhaching Fraud Detection Through Auditor Religiosity, Computer Assisted Audit Techniques, and Task Specific Knowledge: The Moderating Impact of Big Data on Auditors in BPKP, Sumatera Island

DOI:

https://doi.org/10.23917/reaksi.v9i3.6424Keywords:

Auditor Religiosity, Computer Assisted Audit Techniques, Task Specific Knowledge, Big Data, Fraud DetectionAbstract

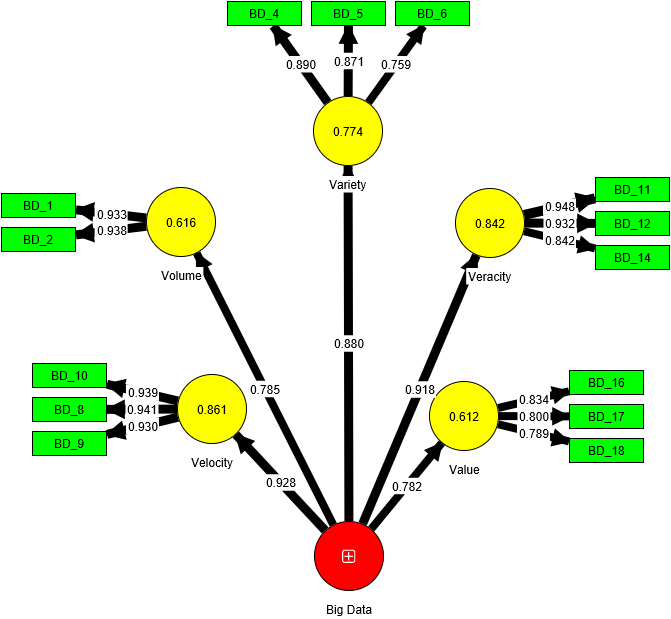

This study investigates the impact of Auditor Religiosity, Computer Assisted Audit Techniques (CAATs), and Task Specific Knowledge on Fraud Detection, with Big Data serving as a moderating variable. Conducted at the Representative Offices of the State Development Audit Agency in Sumatera, the associative research utilized primary data from 220 questionnaires, analyzed via Partial Least Square Structural Equation Modeling (PLS-SEM). Findings reveal that Auditor Religiosity and Task Specific Knowledge significantly influence Fraud Detection, while CAATs do not. Additionally, Big Data does not moderate the effects of Auditor Religiosity and Task Specific Knowledge on Fraud Detection (homologizer moderator). However, Big Data moderates (strengthens) the influence of Computer Assisted Audit Techniques on Fraud Detection (pure moderator).

Submitted

Accepted

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Riset Akuntansi dan Keuangan Indonesia

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.