Voluntary Disclosure: The Role of Institutional Ownership as a Moderating Variable Between Carbon Emission Disclosure to Financial Performance

DOI:

https://doi.org/10.23917/reaksi.v8i3.3060Keywords:

rbon Emission Disclosure, Financial Performance, Institutional OwnershipAbstract

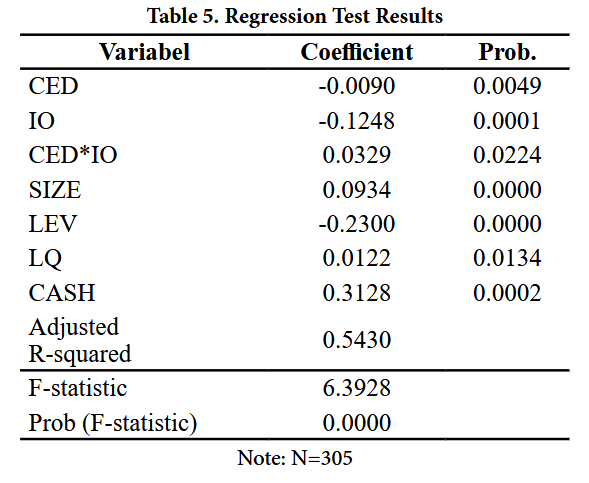

Voluntary disclosure, especially disclosure of carbon emissions in mining companies, is still low. The purpose of this study is to analyze the impact of carbon emission disclosure on financial performance and to find out whether the ownership of institutions can moderate the impact of carbon emission disclosure on financial performance. The data for this study was collected from annual reports and sustainability reports. The sample for this research is 305 mining companies and transportation companies listed on the Indonesia Stock Exchange and Malaysia Stock Exchange in 2018 - 2022. The research model used is moderated regression analysis (MRA). The research results show that carbon emission disclosure has a negative effect on financial performance and institutional ownership can moderate the effect of carbon emission disclosure on financial performance. Disclosure of carbon emissions is so expensive that some companies do not disclose it. Disclosing information about carbon would be an advantage for companies.

Keywords: Carbon Emission Disclosure, Financial Performance, Institutional Ownership.

Submitted

Accepted

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Riset Akuntansi dan Keuangan Indonesia

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.