Mapping of Measurement Accounting Conservatism and Research Opportunity -A Systematic Review

DOI:

https://doi.org/10.23917/reaksi.v8i3.2606Keywords:

accounting conservatism, measurement, accrual basis, market value basis.Abstract

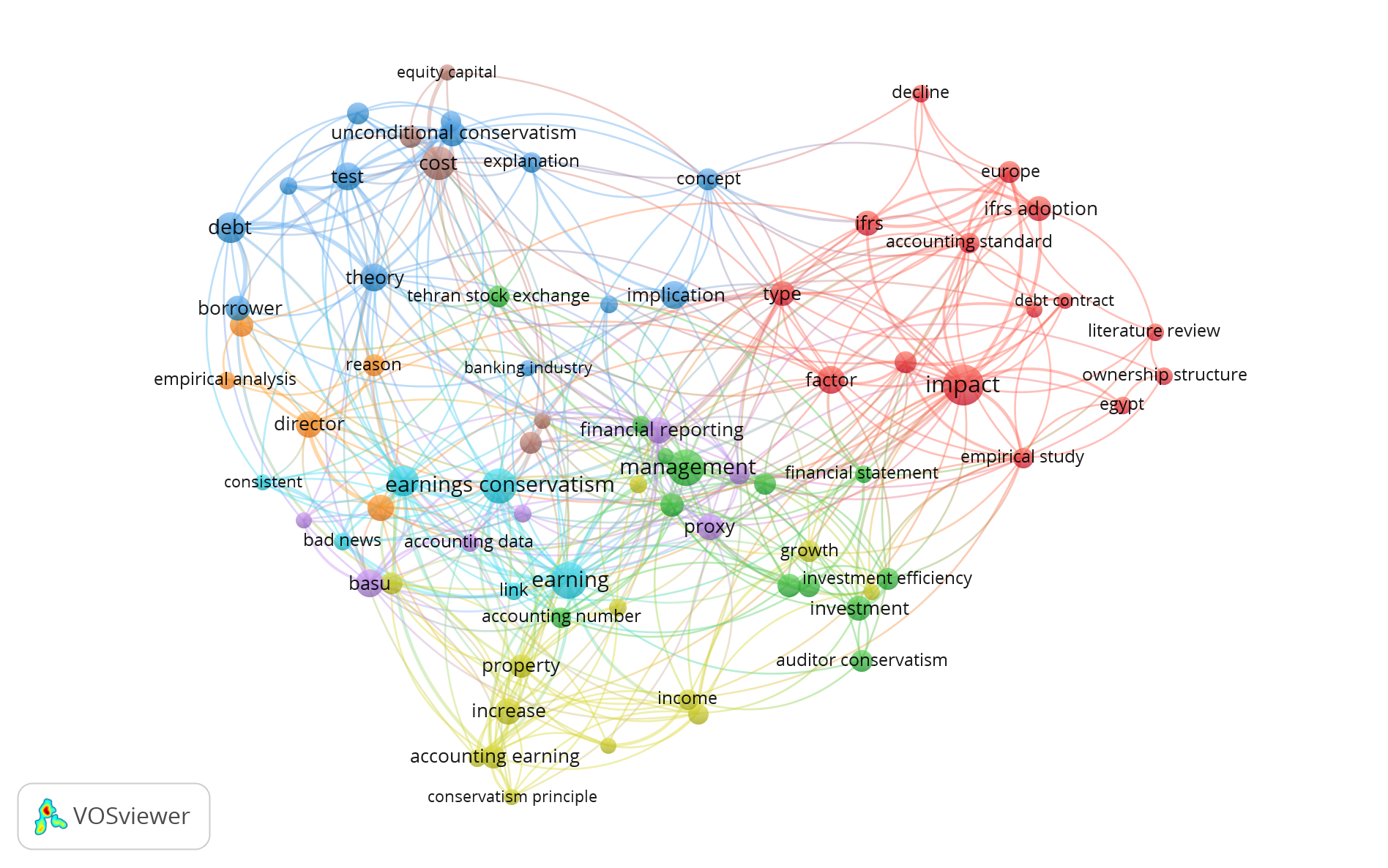

This paper reviews the field of accounting conservatism measurement and the development of research on accounting conservatism measurement, so it is useful to develop insight into the emerging accounting conservatism measurement and outline future research opportunities. This is because research on accounting conservatism uses various measurements. The research method used is a qualitative method systematic literature review approach based on 22 research articles for the period 1999-2022. The research method includes attribute dimensions, data collection techniques and data analysis. The results found that there are three bases for measuring accounting conservatism, namely: accrual-based, market value-based and combined accrual and market value-based. Until now, the use of combined accrual and market value-based measurement dominates, compared to accrual and market value-based. This study found the most widely used accounting conservatism measurement and accounting conservatism measurement trends, while previous studies have not provided an explanation of this. So that future research can analyze why these measurements were used by previous researchers. This research can contribute to the science of financial accounting, especially related to the topic of accounting conservatism.

Keywords: accounting conservatism, measurement, accrual basis, market value basis.

Submitted

Accepted

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Riset Akuntansi dan Keuangan Indonesia

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.