The Embodiment of Corporate Social Responsibility in Sharia Enterprise Theory

DOI:

https://doi.org/10.23917/jisel.v6i1.21134Keywords:

sharia enterprise theory, Islamic commercial bank, social responsibilityAbstract

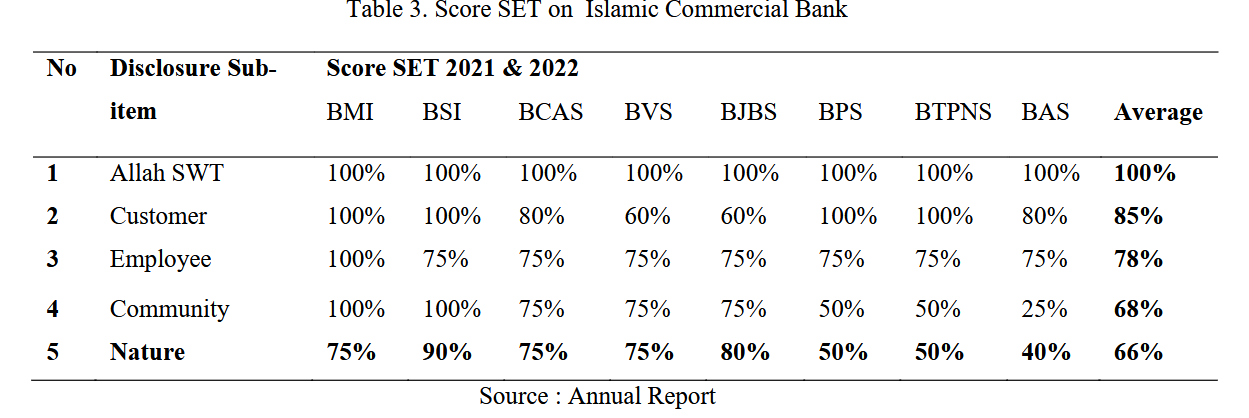

The issue of disclosure of social responsibility by entities is a theme that has always been debated. This is none other than because the implementation of social responsibility disclosures carried out by companies to date still shows a real impact. It is only natural that stakeholders still question its reality. Answering the doubts of these stakeholders, the company's social responsibility began to become a concern. As proof of the accountability activities that have been carried out, this research is here to explore corporate social responsibility accountability based on the Shariah Enterprise Theory (SET) index. Using the research objects of in Indonesia, this research examines the annual reports published by 8 Sharia commercial banks in Indonesia as a source of data. With descriptive qualitative methods through conten analysis as an analysis knife to answer the formulation of the problem, namely how the level of disclosure of social responsibility that has been carried out using the Shariah Enterprise Theory (SET) index. The results of the study proved that 8 in vertical accountability to Allah showed that it was in accordance with the components and criteria that had been set in the Shariah Enterprise Theory (SET) index, while accountability to customers, accountability to employees and accountability to nature as a whole in reporting did not fully meet the components Shariah Enterprise Theory (SET) index. Especially in accountability to nature, it is still far from the component of Shariah Enterprise Theory (SET) index.

Downloads

Submitted

Published

How to Cite

Issue

Section

License

Copyright (c) 2023 Journal of Islamic Economic Laws

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.