Perspectives of Quraish Shihab and Yusuf Qaradhawi on Usury and Interest in the Context of Islamic Finance

DOI:

https://doi.org/10.23917/jisel.v7i01.3189Keywords:

Bank Interest, Comparison, UsuryAbstract

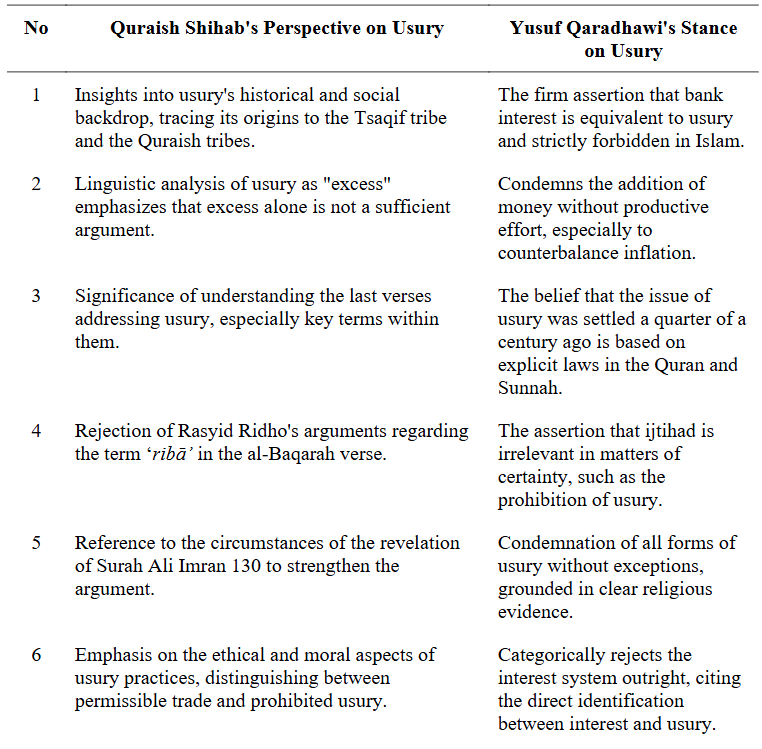

This research explores the perspectives of Quraish Shihab and Yusuf Qaradhawi on the concepts of usury and interest in the context of Islamic finance. Through a literature review methodology, the study provides a descriptive analysis of their viewpoints as presented in various sources, such as books, scholarly works, and related literature. Quraish Shihab's perspective revolves around the intrinsic injustice associated with prohibited usury. He contends that usury involves elements of oppression, exploitation, and duplication, emphasizing the simultaneous taking of excess with debt. Quraish Shihab's view positions usury as a system that perpetuates injustice through its exploitative nature. In contrast, Yusuf Qaradhawi offers a different interpretation, characterizing bank interest as an additional value determined by the payer. Yusuf Qaradhawi introduces a pragmatic dimension by highlighting that, in the case of non-repayment, the debt's amount increases at the specified payment time. This perspective suggests a more flexible approach, where interest is seen as a consequence of delayed repayment rather than an inherently unjust practice. In analyzing the abstractions presented by both scholars, this research unravels the complexities within Islamic finance. It reveals the nuances between Quraish Shihab's emphasis on the inherent injustice of usury and Yusuf Qaradhawi's more practical approach, considering interest as a result of delayed repayment. Through this comparative study, the research contributes to a more comprehensive understanding of the diverse perspectives within the Islamic financial framework.

Downloads

Submitted

Accepted

Published

Versions

- 2024-02-18 (3)

- 2024-02-17 (2)

- 2024-02-17 (1)

How to Cite

Issue

Section

License

Copyright (c) 2024 Journal of Islamic Economic Laws

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.